Climate change increases the frequency and intensity of climate-related hazards, posing a greater risk to individuals, businesses, and communities. Today, extreme weather events, such as droughts and floods as well as slow-onset processes, such as sea level rise and biodiversity loss already cause widespread losses and damages. The Sixth Assessment Report by the Intergovernmental Panel on Climate Change (IPCC) emphasizes that around 3.3 to 3.6 billion people live in circumstances that make them highly vulnerable to climate change. According to Munich Re, climate and disaster induced economic losses and damages worldwide amounted to US$ 270 billion in the year of 2022 alone, with a concerning upward trend. Up to date, funding for disaster response and recovery still largely takes place when the disaster has already occurred, leading to an insufficient and late provision of funds. As a consequence, economic losses from a disaster increase and often divert funds from long-term development action and governmental budget plans to short-term reactive measures to limit the consequences of the disaster. However, this jeopardizes the international achievements of the UN Sustainable Development Goals (SDGs) and general self-determined development of countries.

CDRFI aims to tackle this issue of ad hoc budget reallocations and inefficient action when the disaster has already happened by prearranging financial mechanisms in an anticipatory manner. Pre-arranged finance addresses the needs before a disaster occurs and provides the necessary liquidity even before or just after a disaster. CDRFI instruments can provide this quick and reliable funding in the case of a catastrophic extreme event, thereby lowering the overall impacts of disasters by securing the necessary funds in a cost-efficient way. The InsuResilience Global Partnership (IGP) states that CDRFI can transform disaster response from reactive crisis management to proactive risk management. This paradigm shift from ex-post to ex-ante disaster risk management is crucial.

CDRFI encompasses a broad array of public and private financial instruments and fiscal planning methods that strengthen financial resilience and provide financial protection. The instruments can be applied at the macro, meso, and micro level, providing solutions for national governments, municipalities, businesses, communities, and individuals. CDRFI enables these actors to allocate financial resources towards swift response, efficient relief, and effective recovery efforts. This proactive approach enhances disaster preparedness by strengthening risk management capabilities to better anticipate and manage future challenges. Therefore, appropriate, and cost-effective CDRFI instruments should be incorporated into national disaster risk management strategies and response plans, thereby reducing the strain on budgets, and providing predictable and secure access to funds, while the timely payouts also significantly reduce the follow-up costs of disasters, accelerate economic recovery, and avert the danger of people sliding into poverty.

However, CDRFI should only be applied to what is called “residual risk”, the risk that persists after the implementation of different adaptation measures. While these measures aim to minimize the potential impacts of disasters, they cannot eliminate neither the probability of occurrence nor the damage. By integrating CDRFI instruments with adaptation measures, a comprehensive approach to managing climate risks emerges, strengthening the resilience of communities and economies against the uncertainties that remain even after proactive steps are taken.

Examples of relevant CDRFI instruments include a wide range of insurance schemes, bonds for which repayment can be reduced or suspended in a disaster situation (catastrophe bonds) or pre-arranged loans from multilateral development banks with more favourable conditions than ad-hoc loans (contingent credit), among others. Pre-arranged finance therefore provides not only quick liquidity which increases response preparedness and hence indirectly contributes to risk reduction efforts, but also enables governments to estimate potential disaster-related expenditures more accurately. This predictability allows for better allocation of resources and improved long-term budget planning, as governments can allocate funds for disaster response and recovery in advance.

To ensure adequate and rapid access to financial resources in the event of a disaster, it is crucial to establish CDRFI instruments beforehand. These financial instruments operate at different levels, including micro, meso, and macro.

The following section provides a short overview with two tangible examples of climate risk insurance as a micro instrument and contingency credit as a macro instrument.

Climate Risk Insurance

Climate Risk Insurance (CRI) is an instrument that increases resilience to climate and disaster risks by transferring the risk that remains after all mitigation and adaptation efforts to the local or international insurance markets [referred to as “residual risk”]. CRI contributes to increasing risk awareness and incentivizes adaptive and risk reducing behaviour.

An example of CRI is index-based insurance, where the payout is based on a predetermined quantifiable measure (an index). The index is based on objective weather-related measures like wind speed or rainfall amounts. When the index is triggered (e.g., there is excess rainfall), the pre-determined payout can be distributed timely. Due to lower administrative fees than conventional indemnity insurance schemes (where actual damages are assessed on the ground and hence are in comparison more labour intensive), index-based insurance can be more accessible, especially for rural households.

Index-based insurance can be offered at the micro-level directly to individual households or micro, small, and medium enterprises (MSMEs). It can also be offered at the meso-level to provide portfolio coverage to microfinance institutions (MFIs) or protect agribusinesses’ investments in productivity. Lastly, index-based insurance at the macro level aids sovereign governments or international organizations in preparing for catastrophes and disaster recovery efforts.

Index-based insurance, however, are exposed to basis risk (that is, the risk of a mismatch between actual loss and the payout which is based on the trigger) and only covers selected perils.

One example of climate risk insurance on the micro-level is the “DeRisking Coffee in the Central Highlands” program in Vietnam which was designed in close cooperation between Alliance of Biodiversity International and CIAT (ABC), University of Southern Queensland (USQ) and ECOM Sustainable Management Services. This insurance scheme is designed for coffee farmers and agribusinesses to better protect their crop yields against drought and extreme rainfall perils. During the product development, the farmers participated in the co-design of the product, contributing to their ownership and the long-term success of such a scheme.

Contingent Credit

A contingent credit is a financial instrument used at the macro-level designed to provide quick funding to countries in the direct aftermath of a disaster. The scheme enables governments to immediately access funds under pre-negotiated and pre-approved terms and costs, often more cost-effective than ad-hoc lending following a disaster while also bypassing lengthy approval processes. The purpose of this credit is to aid in humanitarian relief efforts, restore basic services, and repair critical infrastructure. However, this credit is based on prior agreements limiting its disbursement to certain types and intensities of disasters, hence the loans are only provided if the predefined event occurs. Further, contingent credits help to establish better disaster risk management plans as the access to credit is reliant on pre-defined distribution plans which outline how the funds will be utilized. In this regard, contingent credit lines fit into larger sovereign risk management efforts, encouraging proactive planning instead of ex-post response and engaging stakeholders in the disaster risk management agenda.

For instance, in 2021, the World Bank’s Board of Directors approved a Third Disaster Risk Management Development Policy Loan with worth USD 300 million for the Colombian government. The Catastrophe Deferred Drawdown Option (CAT DDO) aims to reduce the country’s fiscal vulnerability to natural and climate-related disasters, but also includes disease outbreaks as a possibility to draw the option. Colombia has used the previous CAT DDOs (I and II) during the La Niña phenomenon in 2010-2011 and the Covid-19 pandemic. This financial instrument allows to draw down the loan at any time over three years and can be extended up to four times for a maximum of 15 years.

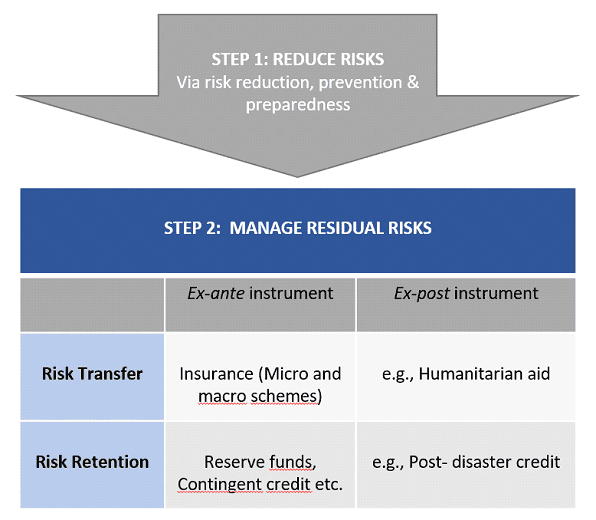

Despite the efforts of mitigating greenhouse gas emissions and of reducing, preventing, and adapting to climate change and the corresponding disasters, risks can only be avoided partially, and residual risks remain. This is where CDRFI plays a critical role by enabling residual risk management through retention and transfer measures. Risk retention refers to the strategy that an individual or an organization bears the risk for potential financial losses and damages resulting from disasters. This may involve proactively earmarking funds to cover such losses or maintaining the flexibility to access loans when needed. On the other hand, risk transfer refers to the actual process of transferring the potential financial burden of disasters to local or international financial markets and thus to another entity, typically through insurance and reinsurance. The insurance policy holder can thereby exchange the risk of unpredictable and potentially high expenses in return for the plannable returning cost of an insurance premium.

CDRFI instruments are vital for climate risk management and adaptation as it provides financial mechanisms to address the impacts of climate disasters. The graph below illustrates the use of CDRFI instruments in residual risk management.

Figure 1: CDRFI instruments as part of residual risk management. (Source: Own illustration based on InsuResilience)

To ensure a successful and cost-efficient integration of CDRFI with climate risk management and (national) disaster risk financing strategies, it is essential to consider both the frequency and severity of these extreme events and disasters using a risk layering approach. Risk layering structures risks and allocates an efficient combination of CDRFI instruments to the specific disaster risks layer. This approach facilitates the cost-effective combination and usage of these instruments, thus increasing financial resilience of a country.

Figure 2: Risk layering and disaster risk financing strategy. (Source: Ghesquiere and Mahul (2010))

To understand better how a risk layering approach works consider the graph above illustrating the relationship between frequency and severity of disasters. The graph shows that events with severe impacts typically occur less frequently compared to events with lower severity. Consequently, the risk layering strategy is structured based on these two factors, with each layer being addressed using specific CDRFI instruments. For instances of high frequency and low severity events, risk retention instruments, including government reserves, contingency budgets, and loans are strategically employed. Conversely, for low frequency but high severity events, risk transfer instruments such as insurance, sovereign risk pools, and catastrophe bonds come into play. This layered approach ensures a nuanced and effective response tailored to the diverse characteristics of disasters.

Finally, CDRFI incentivizes and unlocks additional investments in adaptation measures, such as climate-resilient infrastructure, agriculture, and other sectors, which in turn contribute to enhanced resilience against disasters. The increased resilience vice-versa lowers the cost for risk premiums of the CDRFI schemes, making pre-disaster preparedness more attractive.

The use of CDRFI instruments has substantially grown over the past years and is also well-reflected in international policy climate frameworks that highlight the role of CDRFI in offering financial protection against climate-related disasters and the associated losses and damages. Global policy frameworks -such as the Sustainable Development Goals (SDGs) of the United Nations, the Sendai Framework for Disaster Risk Reduction, the Paris Agreement, and the Warsaw International Mechanism on Loss and Damage acknowledge the urgent need to address climate-related challenges to keep promoting sustainable development. Further, these international climate frameworks aim to proactively manage climate and disaster risks instead of merely addressing their impacts in the aftermath. CDRFI therefore plays a crucial role in facilitating this shift, as these instruments enable the mobilization of funds to finance adaptation efforts, especially in regions at risk [see study: “Climate risk insurance for reslience: Assessing countries’ implementation plans“].

In essence, international climate frameworks recognize the intrinsic link between climate change, disasters, and development. They underscore the importance of coordinated global efforts, financial assistance, and policy integration to address climate risks and create a more resilient and sustainable future for all.

Sustainable Development Goals

Using Climate and Disaster Risk Finance and Insurance can contribute to achieving several SDGs, the most relevant being SDG 1 (No Poverty) and SDG 13 (Climate Action). CDRFI contributes to SDG 1 by providing financial protection to those in need and prevents people from slipping into poverty due to the impacts of disasters, while also being closely linked to SDG 13 as it aims to address the economic impacts and challenges caused by these climate-related disasters.

Sendai Framework

The Sendai Framework, adopted in 2015, is a global agreement that aims to reduce disaster risk and build resilience to disasters, underlining the strong linkages between disasters and climate-related extreme events, and reflecting a major shift from the traditional emphasis on disaster response to disaster risk reduction. Priority three of the framework (Reduce direct economic loss in relation to Gross domestic product) highlights the importance of investing in disaster risk reduction to enhance resilience. In this priority, there is a particular focus on promoting disaster risk transfer and insurance mechanisms.

Paris Agreement

The Paris Agreement represents a global commitment to ambitious and effective climate action. One of its long-term goals is to provide financing to developing countries to mitigate climate change, strengthen resilience against disasters, and enhance abilities to adapt to climate impacts. The agreement calls for enhanced financial support, technology transfer, and capacity-building to assist developing nations in addressing climate risks.

Loss and damage is anchored in the Paris Agreement and refers to the adverse impacts of climate change that go beyond what can be mitigated or adapted to. The provisions for loss and damage are primarily found in article 8 of the agreement, recognizing the importance of averting, minimizing, and addressing losses and damages associated with the adverse effects of climate change, and calling for enhanced understanding, action, and support. Even though there is no agreed upon definition of averting, minimizing, and addressing loss and damage, one could broadly cluster it in the following manner: Averting losses and damages refers to climate change mitigation, whereas minimizing refers to climate change adaptation, which further reduces climate risk. Lastly, addressing loss and damage summarizes all actives meant to respond to materialized climate impacts. CDRFI instruments are explicitly mentioned as one of the eight areas of cooperation for action and support for averting, minimizing, and addressing loss and damage. They can play a critical role in addressing the economic losses and damages by providing payouts for timely and reliable post-disaster recovery, reconstruction, as well as other resilience-building efforts. However, it needs to be stressed at this point that financial responsibilities and compensation payments due to losses and damages are explicitly excluded in the Paris Agreement.

Figure 3: CDRFI instruments in International Policy Frameworks. (Source: InsuResilience Global Partnership)

The Global Shield – a concrete offer to addressing loss and damage

In the loss and damage context, the Global Shield (GS) against Climate Risks was launched at COP27 in Egypt as an initiative of the G7 under the German presidency together with the Vulnerable Twenty (V20). The aim of the Global Shield is to provide and facilitate more and better pre-arranged protection against climate and disaster related risks for vulnerable people and countries. Greater financial protection and faster and more reliable disaster preparedness and response will contribute to effectively addressing losses and damages exacerbated by climate change. The GS builds on the efforts of the InsuResilience Global Partnership, an initiative Germany has prioritised during its last G7 presidency in 2015. The GS will support countries in acquiring needs-based financial protection in a systematic, coherent, and sustained way, leveraging, and including a diverse range institutions and actors.

Therefore, a central element of the Global Shield structure is the demand-driven so called In-country Process (ICP). The ICP is an inclusive and country-led process, bringing together all relevant CDRFI stakeholders and key governmental actors of the country, as well as the perspectives of vulnerable and marginalised groups. The process identifies already existing CDRFI solutions in the country and conducts a gap analysis, ultimately resulting in the compilation of a concrete protection gap. This enables governments to make informed decisions and to submit a country-tailored requests for CDRFI support to the financing vehicles of the Global Shield at the end of this process, which are then tasked to channel and offer the requested solutions.

You are currently viewing a placeholder content from Vimeo. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Google Maps. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Google Maps. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Mapbox. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from OpenStreetMap. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information